Introduction

A CIBIL score is a numerical reflection of your creditworthiness, typically ranging from 300 to 900. While a high CIBIL score can open doors to better financial opportunities, a low score can make obtaining a personal loan more challenging. But don’t worry—it’s not impossible! You can still secure a personal loan with low CIBIL score.

In this comprehensive guide, we’ll provide actionable tips and strategies for navigating the loan application process, regardless of your credit history.

Also Read: How to Improve CIBIL Score?

What is a CIBIL Score?

Think of your CIBIL score as your financial health report. It shows lenders how responsibly you manage credit. Factors like timely bill payments, maintaining a low debt-to-income ratio, and prudent borrowing habits can increase your score. On the other hand, missed payments, high debt, and frequent loan applications can bring it down.

When applying for loans or credit cards, lenders prioritize applicants with higher CIBIL scores, as it reflects a lower credit risk.

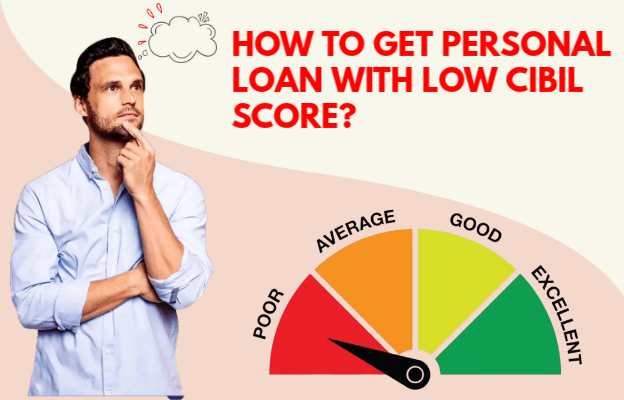

Here’s a breakdown of the CIBIL score ranges and their impact on loan approval:

CIBIL Score Range | Rating | Loan Approval Chances |

750 – 900 | Excellent | Very High |

701 – 749 | Good | High |

621 – 700 | Fair | Moderate |

551 – 620 | Low | Low |

300 – 550 | Very Low | Extremely Low |

Effective Tips to Get a Personal Loan with Low CIBIL Score

A low CIBIL score doesn’t mean your financial aspirations are out of reach. Follow these practical steps to increase your chances of loan approval:

Check and Correct Your CIBIL Report

Start by reviewing your CIBIL report for errors. Mistakes like incorrect personal details or discrepancies in payment history can negatively impact your score. Dispute inaccuracies immediately with the credit bureau to rectify them.

Improve Your Credit Utilization Ratio

Maintain a credit utilization ratio below 30%. For instance, if your credit limit is INR 1,00,000, keep your outstanding credit below INR 30,000. Paying off existing debts can help improve this ratio and boost your credit score.

Build a Positive Payment History

Consistency is key. Pay all your bills—credit cards, utilities, and EMIs—on time. Even small, consistent payments contribute significantly to improving your credit score over time.

Address NA or NH in Your Credit Report

If your credit report shows “NA” (Not Applicable) or “NH” (No History) due to limited credit activity in the past 36 months, explain this to your lender. In some cases, they may approve your loan at a slightly higher interest rate.

Apply with a Co-Applicant or Guarantor

Consider involving a co-applicant or guarantor with a strong credit score. Their financial credibility can offset your low score, increasing the likelihood of loan approval. However, remember that the co-applicant becomes equally responsible for loan repayment.

Opt for a Secured Loan

If you own assets like property, fixed deposits, or a vehicle, you can opt for a secured personal loan. Offering collateral reduces the lender’s risk, making it easier for them to approve your application.

Request a Smaller Loan Amount

Applying for a smaller loan amount reduces the lender’s risk and increases your chances of approval. Evaluate your needs and only request what you can afford to repay.

Also Read: How to check CIBIL Score by PAN Card?

Conclusion

A low CIBIL score doesn’t have to be a permanent hurdle to accessing financial support. By understanding your credit profile, rectifying errors, and adopting responsible financial habits, you can improve your eligibility for personal loans. Lenders may assess additional factors like your income stability and existing liabilities, so present a strong case with complete documentation.

Take proactive steps today to not just secure the loan you need but also build a healthier financial future!

Some Other Important “CIBIL Score” Pages

How to Check CIBIL Score for Free?

How to Get Personal Loans With Low CIBIL Score? FAQs

Can I get a personal loan with a low CIBIL score?

Ans. Yes, it is possible to get a personal loan with a low CIBIL score, though it might come with higher interest rates or stricter terms. Strategies like applying for a secured loan, involving a co-applicant, or requesting a smaller loan amount can improve your chances.

What is considered a low CIBIL score for personal loans?

Ans. A CIBIL score below 621 is generally considered low. Scores between 300-550 are rated as very low, significantly reducing the chances of loan approval.

How can I increase my chances of loan approval with a low CIBIL score?

Ans. You can increase your chances of loan approval with a low CIBIL score by following the below-mentioned points:

- Check your CIBIL report: Identify and correct errors.

- Lower your credit utilization ratio: Keep it below 30%.

- Build a payment history: Make timely payments.

- Apply with a guarantor or co-applicant: Leverage their creditworthiness.

- Opt for a secured loan: Offer collateral to reduce lender risk.

Will lenders charge higher interest rates if I have a low CIBIL score?

Ans. Yes, lenders often charge higher interest rates to offset the risk associated with lending to individuals with low credit scores. Shopping around for better terms can help you secure a more favorable rate.

Can I get a loan without a credit history or with an NA/NH credit report?

Ans. Yes, some lenders provide loans to individuals with no credit history. In such cases, the interest rate may be slightly higher. You can also explain the situation to your lender and present other proof of financial stability.

Are secured loans easier to get with a low CIBIL score?

Ans. Yes, secured loans are generally easier to obtain because the collateral reduces the lender’s risk. Examples of collateral include property, fixed deposits, or vehicles.

Should I apply to multiple lenders simultaneously if my CIBIL score is low?

Ans. No, avoid applying to multiple lenders simultaneously. Each application results in a hard inquiry, which can further lower your score. Instead, research and apply strategically to lenders who are more likely to approve your loan.

Can digital lenders or NBFCs approve loans for low CIBIL scores?

Ans. Yes, many digital lenders and Non-Banking Financial Companies (NBFCs) offer loans to individuals with low CIBIL scores. However, their interest rates may be higher than traditional banks.

How long does it take to improve a low CIBIL score?

Ans. Improving your CIBIL score takes time, depending on factors like your payment history, credit utilization, and existing debts. With consistent efforts, you can see improvements within 6-12 months.

What should I avoid when applying for a loan with a low CIBIL score?

Ans. You should avoid below mentioned things when applying for a loan with a low CIBIL score:

- Multiple applications: Avoid applying to several lenders at once.

- Incomplete documentation: Submit all required documents to strengthen your case.

- High loan amounts: Stick to a manageable loan amount.

- Unsecured loans with high-interest rates: Evaluate options carefully before committing.